A Preface (from our CEO)

Happy New Year 2023!!!

It has been a couple of years since TK Bardwell and I partnered to publish an industry report. With the very volatile conditions we were experiencing, few were prepared to weigh in on predictions as I personally, and likely most of you, have been blown away at some of the things we have seen (and continue to take place) in our industry and economy. In retrospect, who would have thought that the world supply chain could have been completely shut down for such a long period of time? Or that the complete restarting of it would have produced the short-term and long-term effects that it did? The complete inability to predict where we were headed and the barrage of totally unexpected challenges that everyone faced each day were overwhelming. Company leaders were facing, almost daily, a totally new and unexpected challenge most likely never experienced nor predictable, while also trying to manage the day-to-day challenges of running a profitable business.

Whenever drastic changes of this nature take place in our economy, the pendulum swings outside historical norms. But in this time, I personally have been totally amazed as to the degree of the pendulum swing. The demand for labor while the labor participation rate hit historic lows has created a new watershed of the actual minimum wage and benefits, that will most likely never return to previous norms. The changes culturally that have taken place in a post-COVID world has had some positive long-term effects while also building in many negative impacts. Who could have predicted the extreme change in the real estate market that we experienced where families could take advantage of large increases in the equity of their homes and investment properties while also facing the dilemma of replacing the properties that they just sold! Much of the inflationary costs in food and other products were not only impacted by labor inputs, but also the related energy cost inflation we experienced during the last two years. We would like to share some insights on the general economy and freight market specifically with you: our customers, employees, business partners and community.

Greg D. Brown

Chairman and CEO

A general format will follow:

- Introduction and Recap of 2022

- 2023 Economic and Truckload Freight Market Outlook

- Regulations and Other Factors that are Likely to Impact Conditions for 2023

- Final Observations

Introduction and Recap of 2022

2022 in Review

The year 2022 closed as being one of the more successful years for the manufacturing and freight industries. Market conditions have generally been favorable, and pricing and demand have been stable. How much more successful could 2022 have been had conditions been even more favorable? If manufacturing didn’t continue to have supply chain interruptions, if labor had been more available, 2022 truly could have been full throttle. After the government stimulus, we had a robust return to demand for products and services. However, almost every industry had either tremendous challenges keeping the sales and manufacturing processes running without interruption or companies being limited with how much they could realize due to labor constraints. Heading into the New Year, supply chains seemingly are becoming more reliable. However, there has not been much relief on the labor side.

Kiplinger is predicting that “the economy is going to struggle with growth coming in at the weakest in many years outside the sharp downturns of 2020 and 2008-09. The labor market will slowly lose steam, with the number of jobs created down from month-to-month, followed by wage increases proceeding to cool off.” This is a huge reversal as 2022 experienced tremendous gains in jobs being created. It appears that the actions of the Federal Reserve Board are beginning to show measurable impact.

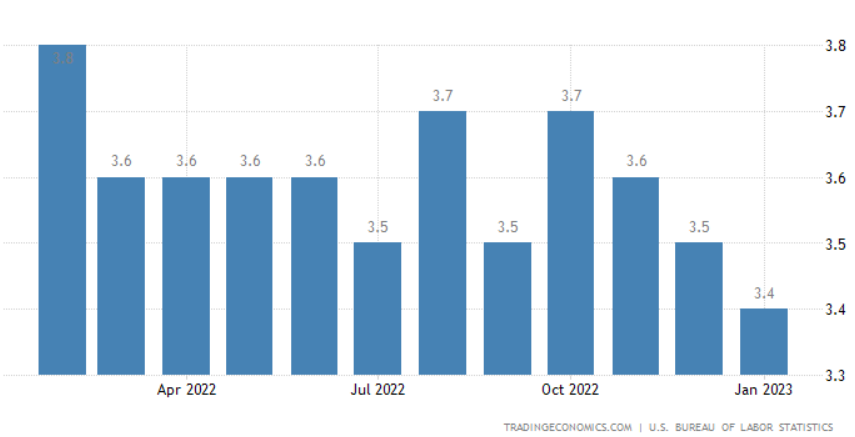

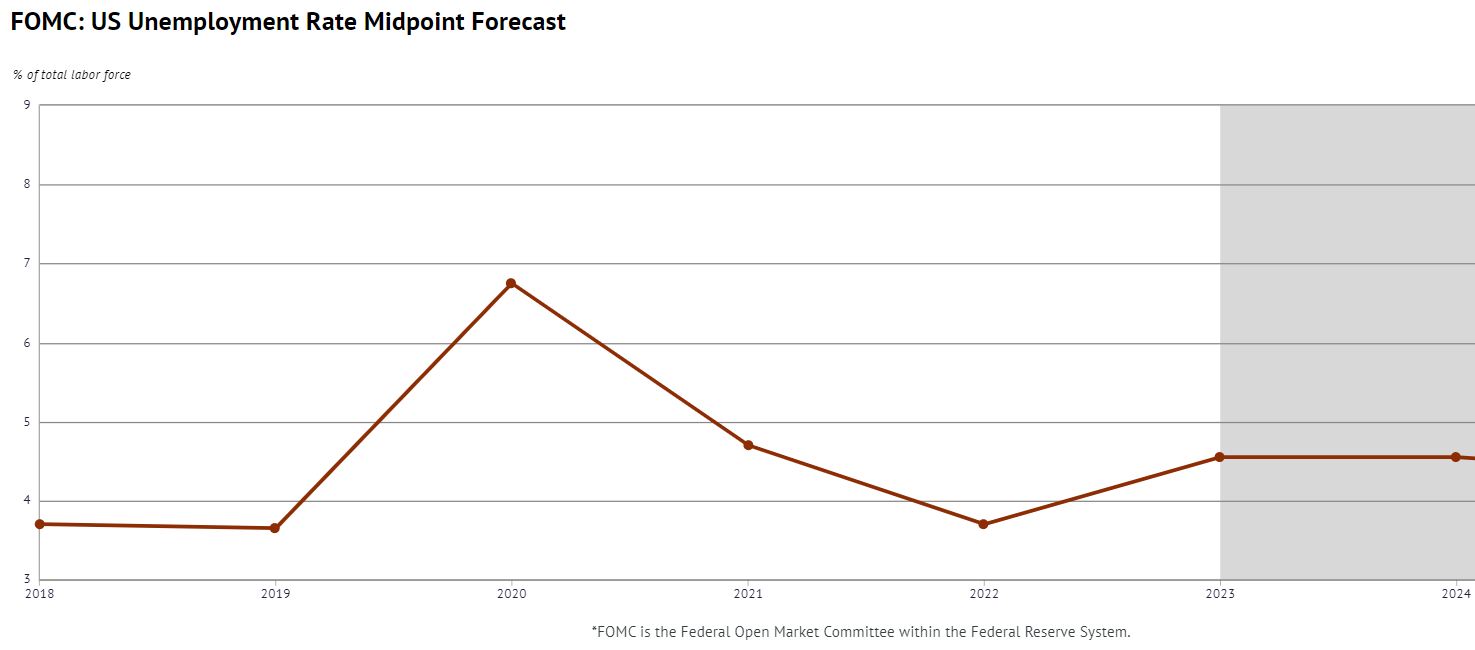

“Full Employment” is defined as “an economic situation in which all available labor resources are being used in the most efficient way possible” and is generally considered to be 4% unemployment. An unemployment rate below 4% may fuel inflation and does not allow for the labor force to flex around fluctuations of demand. 2022 closed at 3.5% unemployment.

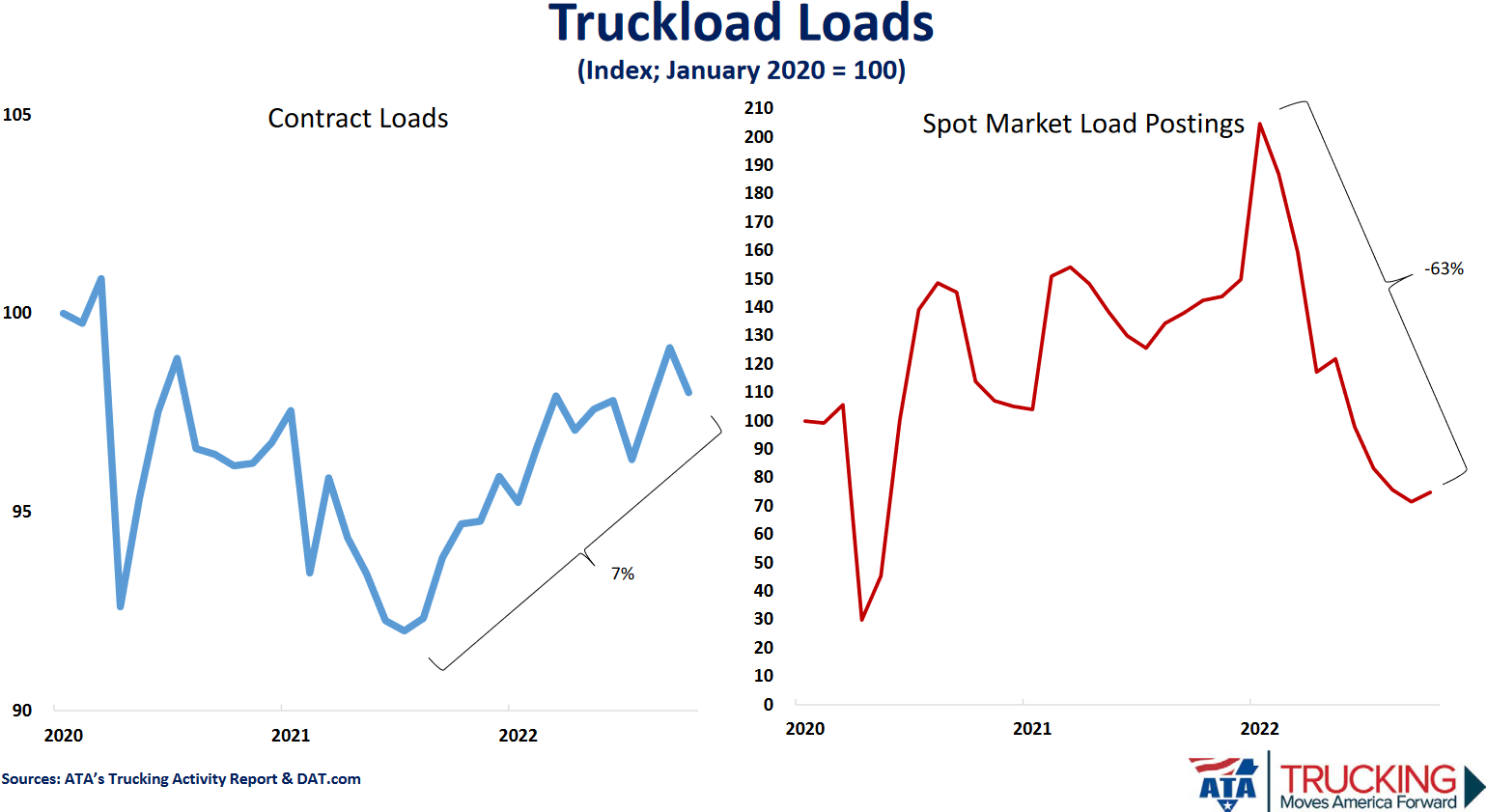

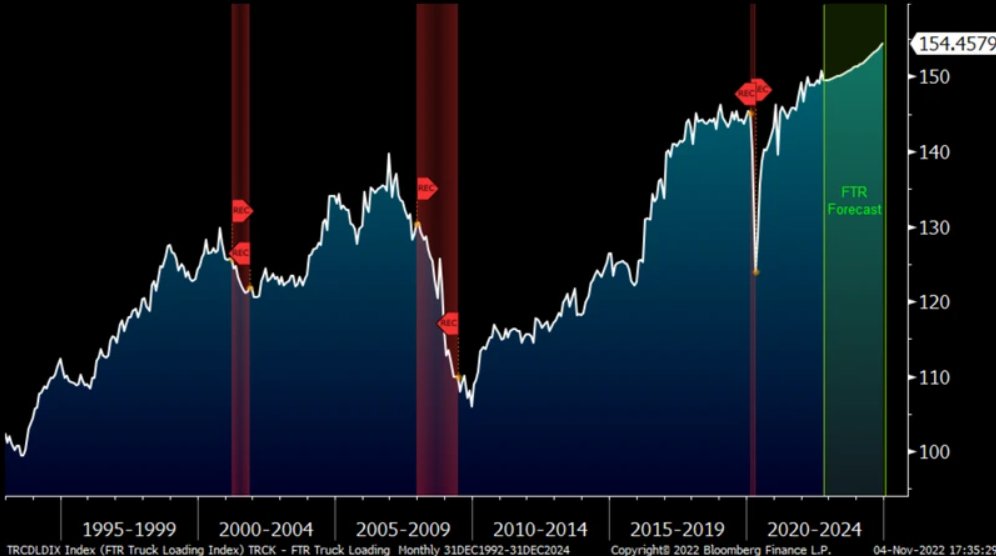

2022 started with exceptionally tight truck capacity and upward pressure on rates before experiencing a dramatic pendulum swing to surplus and the bottom falling out of the spot market in March. Since then, the market has steadily deteriorated. While many economists warned of the inherent uncertainties of a market dependent upon new variables with very little historical precedent, few predicted the freight recession of 2022.

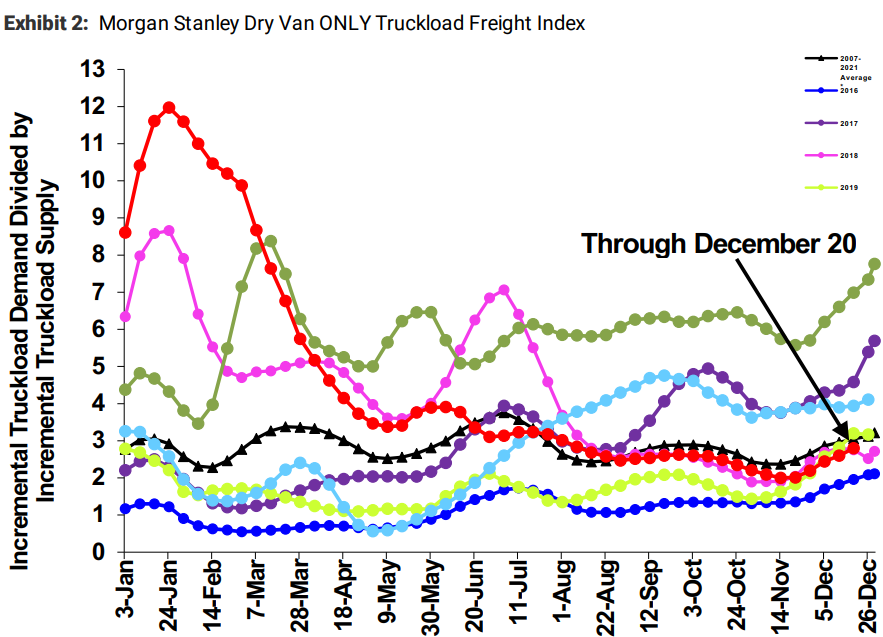

Conventional freight market forecasts center around the confluence of 2 primary factors: supply of seated trucks vs demand for truck capacity. There are hundreds of factors that influence each to varying degrees, but one principle has them nearly perpetually out of sync; demand is very agile while supply takes considerably more time to respond to demand shocks. Companies like Morgan Stanley, FTR Transportation Intelligence and others do a very good job of forecasting. However, when compounded by supply chain disruptions, waning artificial demand, and dwindling labor participation, it was just too many substantial variables to produce an accurate forecast in 2022. Some missed by a mile.

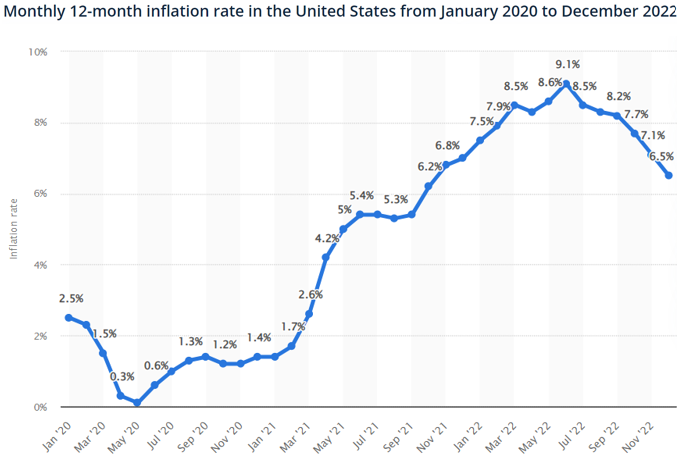

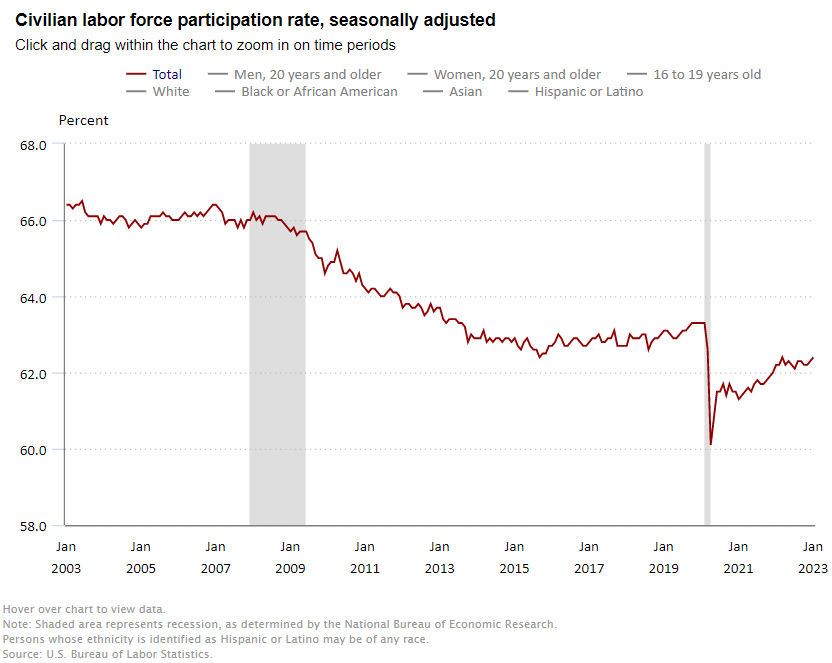

There were, however, a few canaries in the coalmine. The labor participation rate fell from 63.5% at the beginning of 2020 to 60% by the end of 2020, only recovering to 62% as of the most recent measure in November of 2022. That is 5,000,000 that left the labor force and did not return. Simultaneously, various covid-related stimulus programs increased consumer spending and therefore, truckload demand. Thus, fewer goods and services were being supplied but demand for them was artificially inflated. Therefore, too much money was competing for too few goods and services. This is a perfect recipe for inflation.

Inflation began to reduce demand. However, manufacturers continued to produce goods and inventories began to rise dramatically toward the end of 2021 and beginning of 2022. Inventories were drawn down over the next several months and without increases in consumption which did not occur, this reduced demand for truckload capacity.

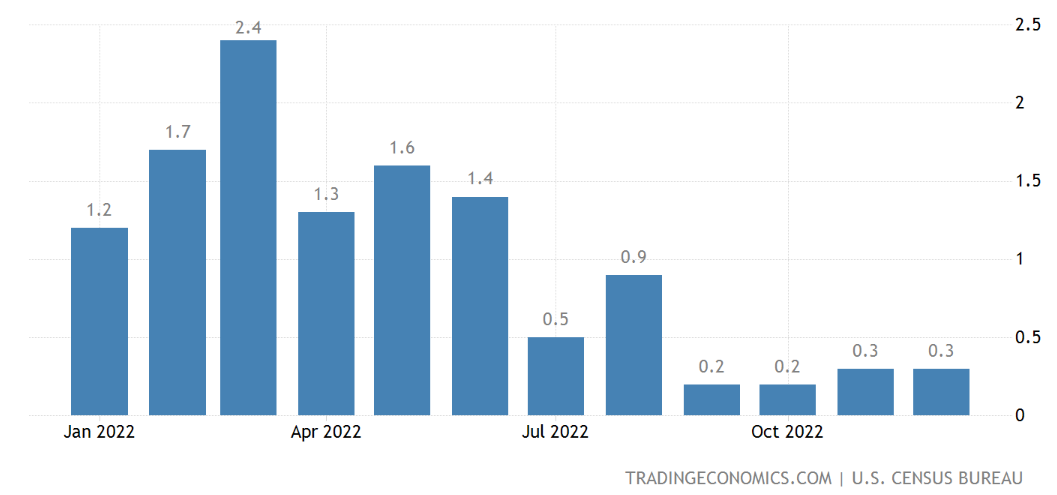

Business Inventories

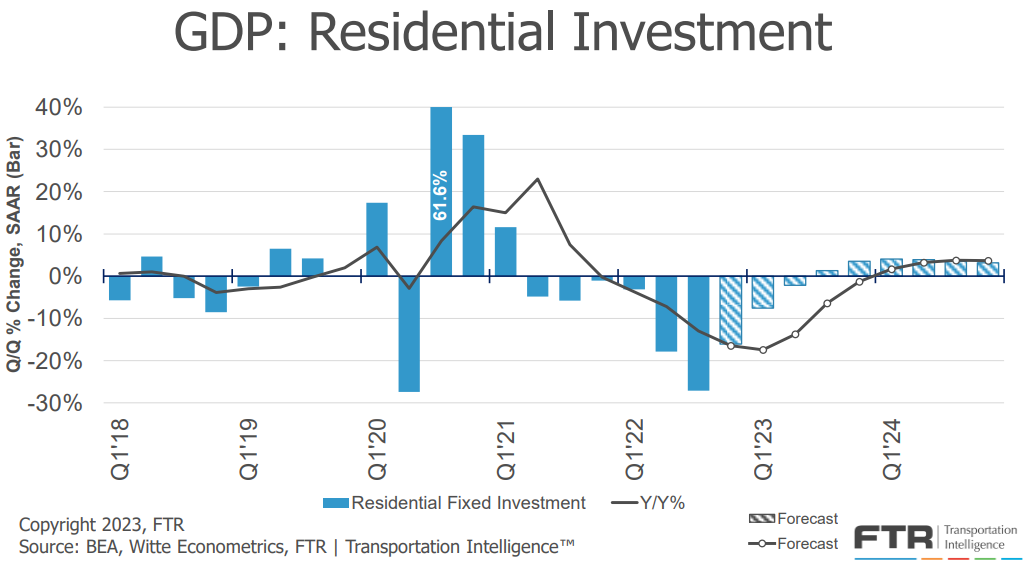

GDP: Residential Investment had fallen for four consecutive quarters leading up to the dramatic Q2 and Q3 decline:

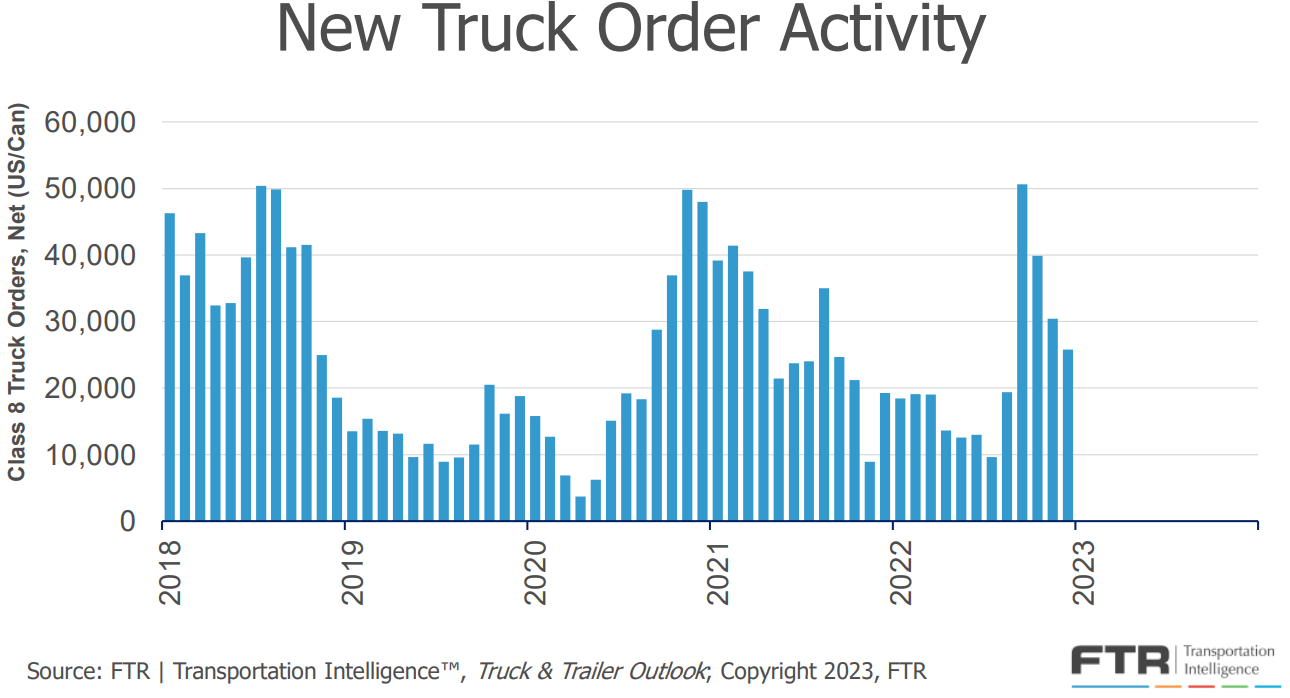

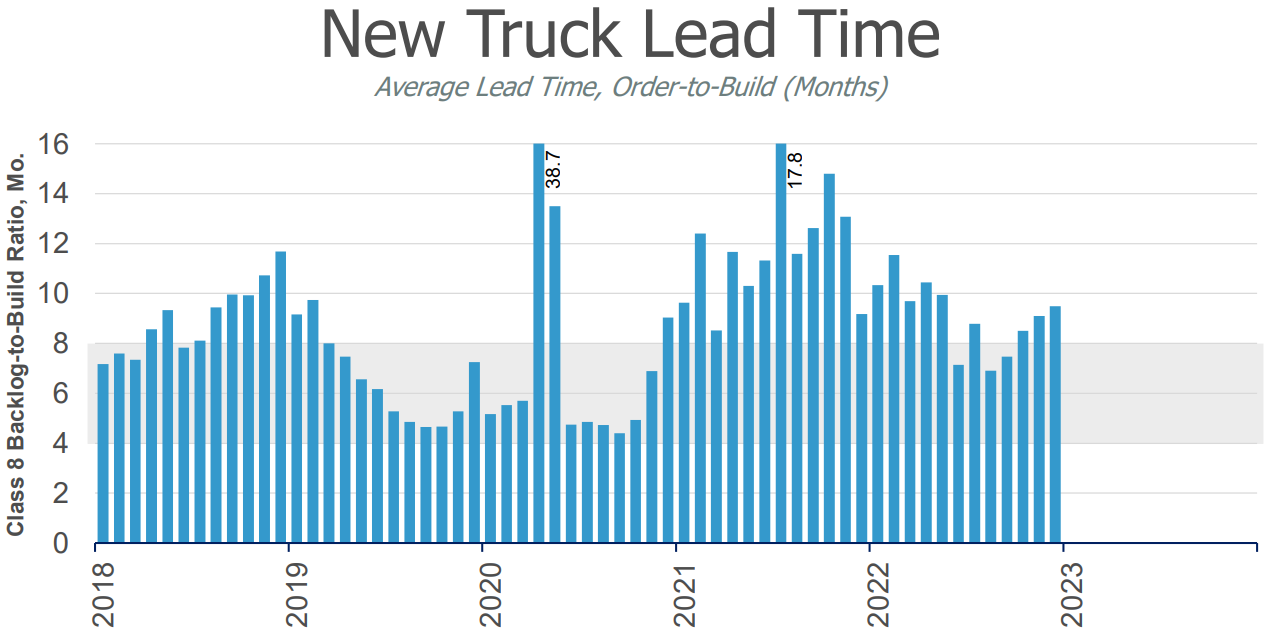

Class 8 truck orders were in excess of replenishment rates between August of 2020 and September of 2021. This, combined with a 12-18 month lead time (see figures under “supply component”), should have foretold of a flooding of capacity into the market during Q1 and Q2 of 2022.

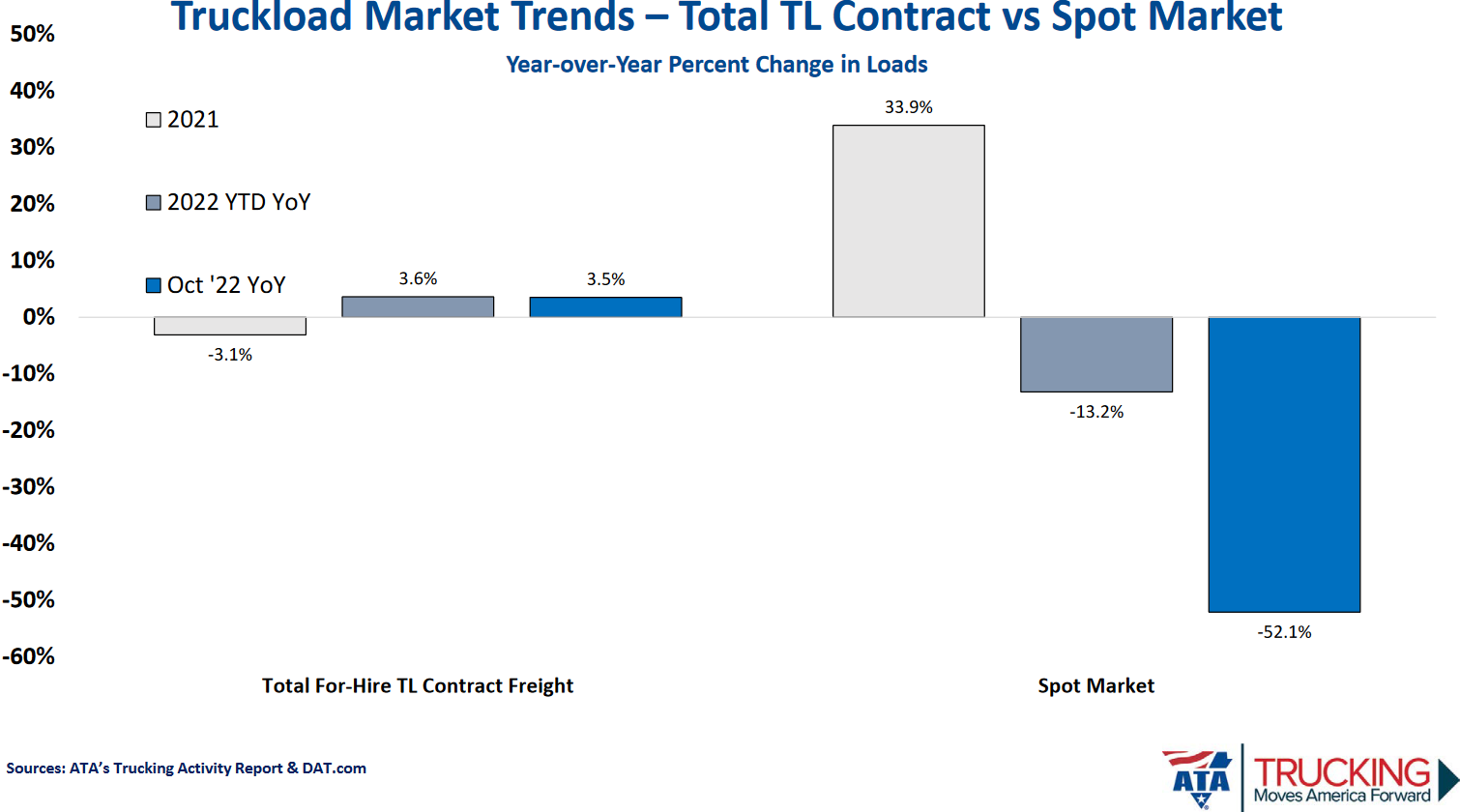

This excess capacity has too many trucks competing for too few truckloads which has created downward pressure on rates. Van contract rates are down slightly but van spot rates are down nearly 40% year-over-year. Reefer contract rates are up slightly but reefer spot rates are down 32% year-over-year. Flatbed contract rates are down slightly and flatbed spot rates are down 20%.

2023 Market Outlook

As best we can, we will attempt to share what we see are the reasonable expectations of what 2023 will bring along with more specific industry insights.

General Economic

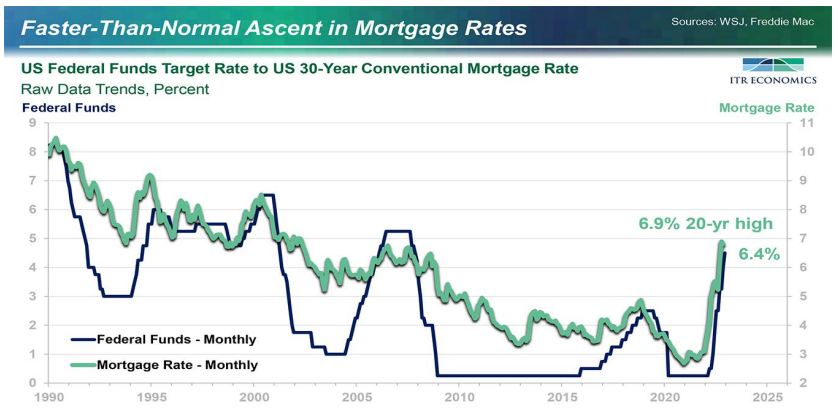

The reality is that the factors of impact in 2022 and the impacts on inflation are lagging, such that continued commitment to interest rate increases in 2023 could accelerate these effects, causing a hard landing for the economy. The effects have already impacted the housing industry, with manufacturing expected to be shortly behind, albeit to a lesser extent. The faster than normal ascent in interest rates, has resulted in a worse than expected affordability issue, according to ITR Economics, and will result in another disappointing year for single family housing.

Inventories are already beginning to climb and the spot market that was white hot twelve months ago in attempting to build those inventories, has already hit recessionary numbers.

Many forecasters suggest that we will actually see mini-recessions hitting one industry and then another, rather than a full-blown broad slowdown. This could be problematic in that it could mask the numbers the Fed watches, and will not provide an accurate view of reality within these industries. It appears that Fed Chair Jerome Powell and his board is committed to staying the course on rate increases until it actually begins to impact wage increases (another lagging indicator), and with current labor markets, this could cause a much deeper trough before those goals can be met and become obvious.

At minimum we should expect continued slowdowns, and eventual recession likely by the end of 2023. The depth and length of this slowdown will most certainly impact 2024. The stock market appears with its recent short-lived and marginal bounce, that it is factoring in that the Federal Reserve will cut back its aggressive rise in rates. However, if Chairman Powell does not see the impacts he desires and continues his current path, another adjustment to the stock market could be coming as well. One ongoing concern is the steady continued decline of the labor participation rate. Until a return to more normal participation rates can be attained, we will continue to have challenges in our labor markets.

General economic data was forewarning of a moderate recession during the first two quarters of 2022. However, a bit of a bounce in Q3 and lukewarm Q4 have moderated some expectations for 2023. Factors are a mixed bag with some sectors expecting some strength (light autos), with others facing serious headwinds (housing). Unemployment is very low and is expected to rise only slightly during 2023.

Because demand for consumer goods exceeded supply during early 2022, the manufacturing outlook was more a function of capacity to meet demand than demand itself. However, demand began waning as inflation drew down savings and disposable income of consumers. Manufacturing forecasts show some light contraction in Q1 and Q2 of 2023.

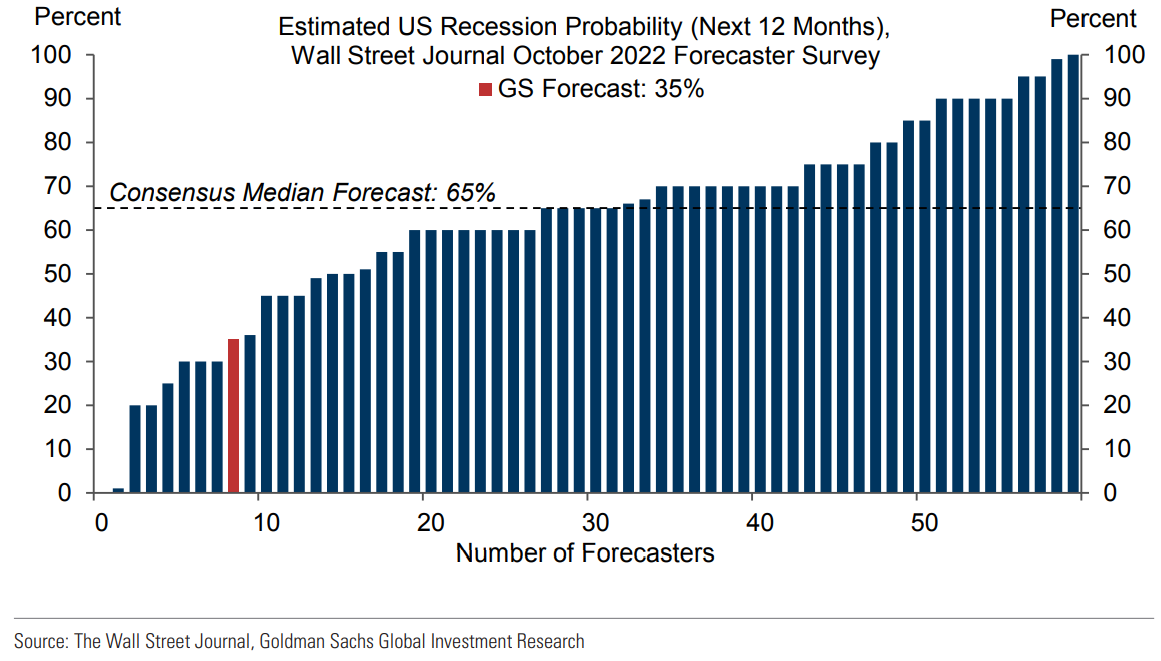

Inflation and the FEDs aggressive strategies to control it have put a damper on GDP growth. However, the forecasts range from “very mild recession” to “modest growth” and a 61% likelihood of recession during 2023. This is an improvement since October and November when the aggregate forecast pegged the likelihood of a recession in 2023 at 65% (pictured below).

Inflation itself will continue its decline as an additional 100-150 bps are expected to be added by the FED by the close of Q2 2023. No rate reductions are expected during 2023 unless the economy slips into recession, in which case, one can conclude that the Fed was too aggressive in their efforts to curb inflation.

2023 Freight Industry Outlook

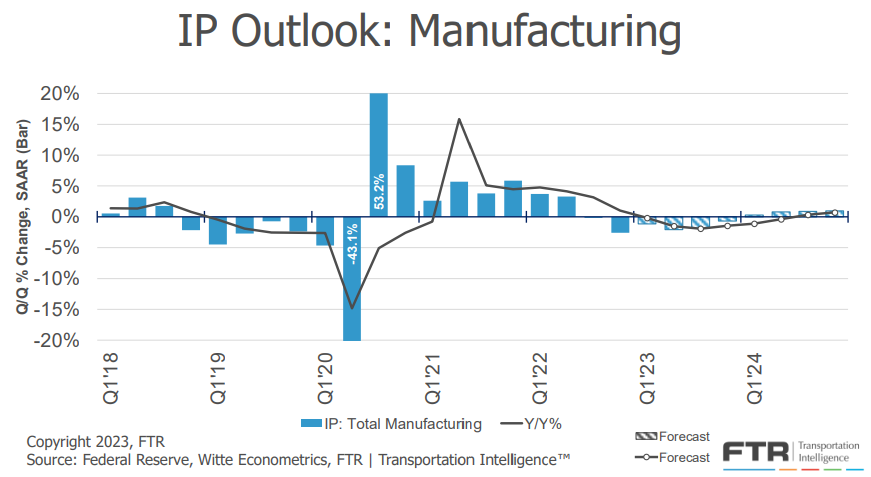

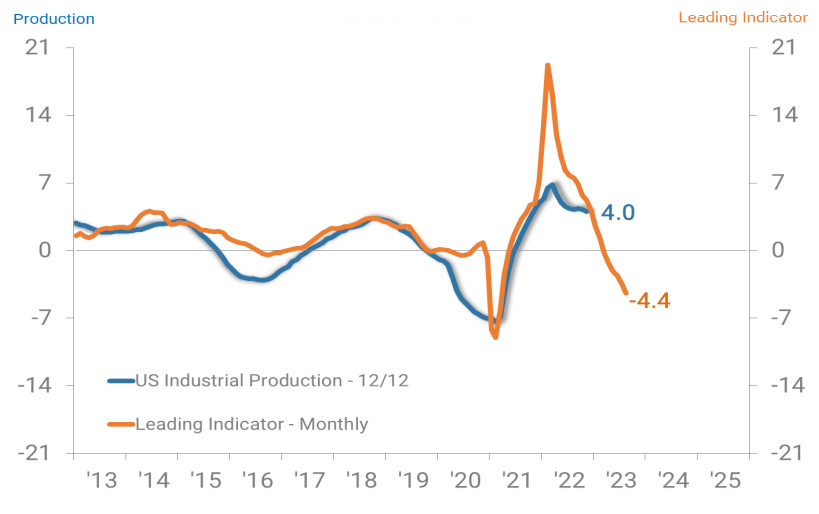

The spot market portion of the freight industry has already entered recession territory. Demand on the contract side has remained stable, however, is most likely to begin some degradation as well throughout 2023. ITR Economics US Industrial Production Leading Indicator chart projects continued decline at least through the end of 2023. The leading indicator is shifted forward eight months in order to project the forward trends.

We also monitor the Bank of America Global Research Industry Overview, where they are predicting that as the Spot Market has led the way with dramatic reductions in demand, they “expect contract rates to decline further into March to May peak bid season as shippers move to secure lower prices”. However, they continue further that this should be the trough, with a return to stabilization and return to more of a positive trend in rate stabilization and firming up, as peak produce season will come in May to June. This year’s produce season impact could be very telling in that for 2022, produce season generated barely a blip. This year’s crops, along with that impact on capacity should provide an early indication as to how the rest of the year could follow.

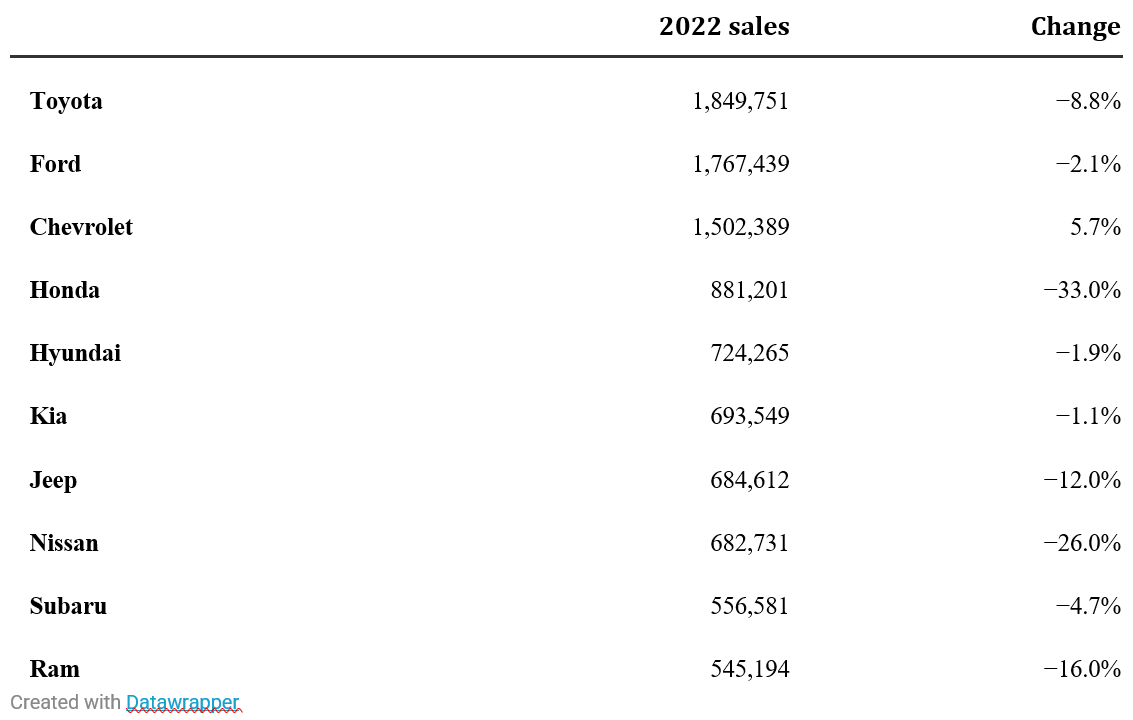

One exception that we have noticed, in our review of multiple forecasts, is that the auto industry should be positioned to have somewhat of a favorable expectation, as there has been much pent-up demand built into the economy due to the inability to produce to meet the appetite for automobiles during 2022. As supply chains have become more dependable, production interruptions have gotten less problematic. As more automobiles begin to find their way to the dealer showrooms, hopefully, the automakers will approach more normal sales levels. 2022 sale levels and YOY change are shown below per Automotive News:

FTR Transportation Intelligence indicates that the U. S. Freight Outlook is “Improved outlooks for loadings related to food and construction – and to a lesser extent, automotive – account for a slightly stronger 2023 forecast through the second half of the year. Total truck loadings are forecast at a 0.6 % increase y/y in 2023.” This is an improvement from their last published forecast. The different segments have the following forecasts from FTR:

Dry Van Loadings – Up 1.3 % y/y

Refrigerated Loadings – Up 1.7 % y/y

Flatbed Loadings – Down 1.5 % y/y

Specialized Loadings – Up 2.1 % y/y

Tank Loadings – Down 0.7 % y/y

Bulk/Dump Loadings – Flat y/y

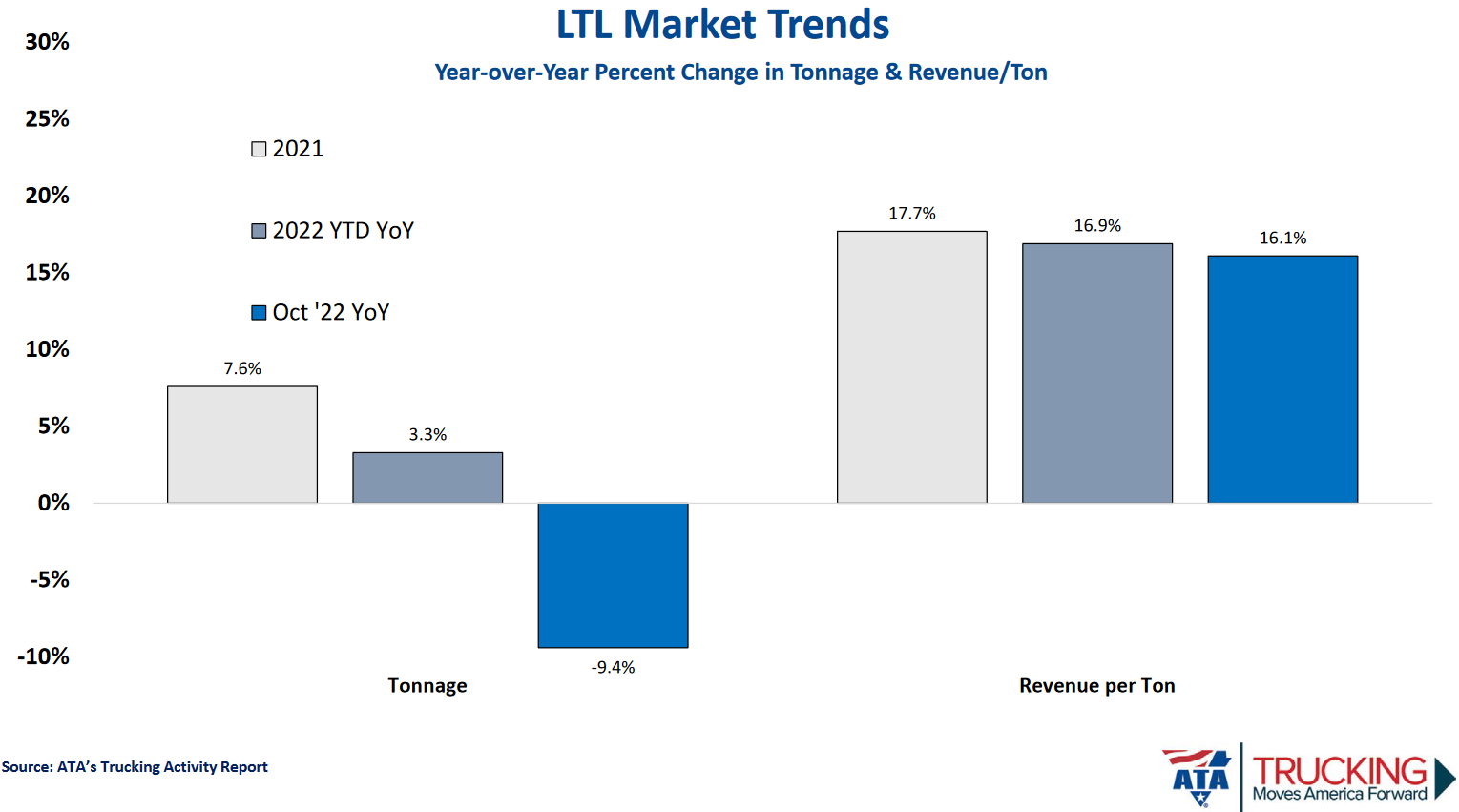

Further, FTR is suggesting, “The forecast for LTL Rates continue to firm modestly but to still be down 1.8% y/y from 2022” as the LTL segment continues to be in flux and adjusting to changing market conditions. Most LTL fleets are actually reducing tractors as a result of this trend.

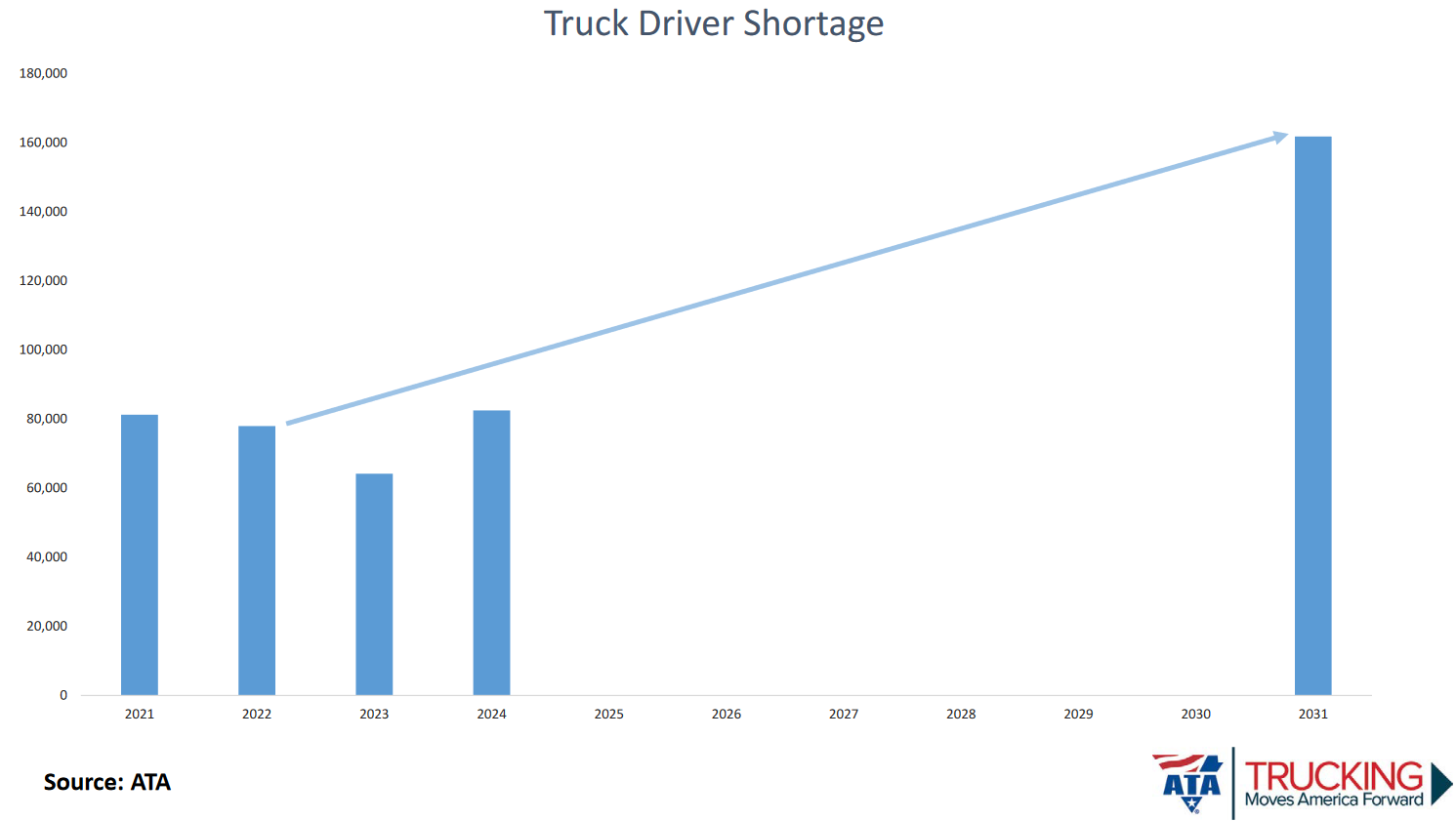

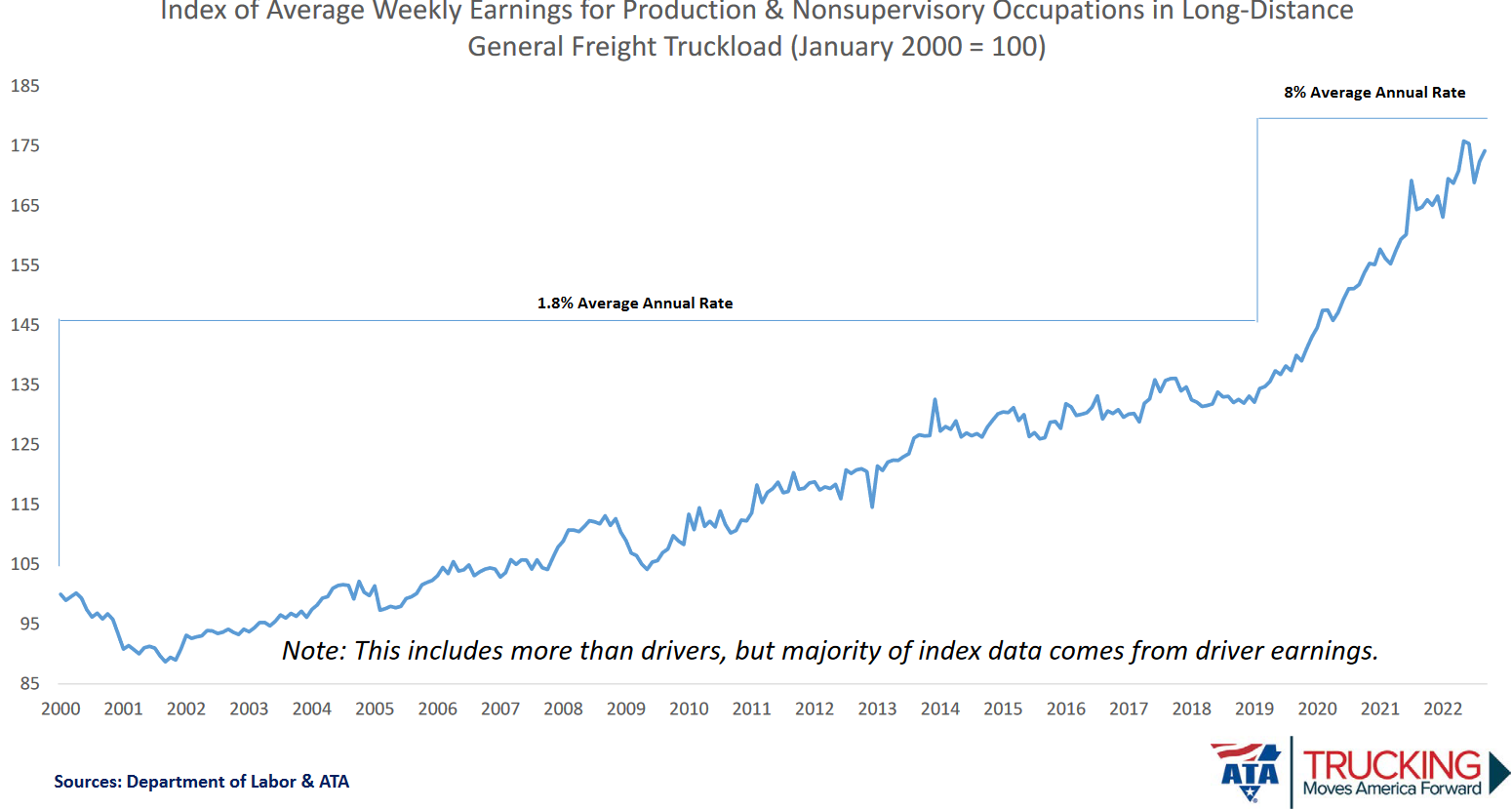

Labor – The elephant in the room for ALL industries have been the availability (or rather the lack thereof) of labor. This is especially true of the freight industry. As demand for freight hit the highest levels in the last 40 years through March 2022, fleets resorted to extreme recruiting ploys to entice drivers from other companies, as the entry of new drivers into our industry are at historic lows, and the exodus of highly productive baby boomers continues. Fleets that have responded with rapid increases in pay and benefits will be faced with the impossible task of walking any of that back. We have reached a new watershed for driver pay in our industry and for the most part, it has been a long time coming. Driver pay has not kept up with comparable pay and benefits in other industries. This problem even if we were to experience a small to moderate recession, it is not expected to get better any time soon. As we can see from the following chart, the truck driver shortage is expected to have some relief during 2023, with a return to 80,000 drivers short in our industry in 2024 but could be double that by 2031.

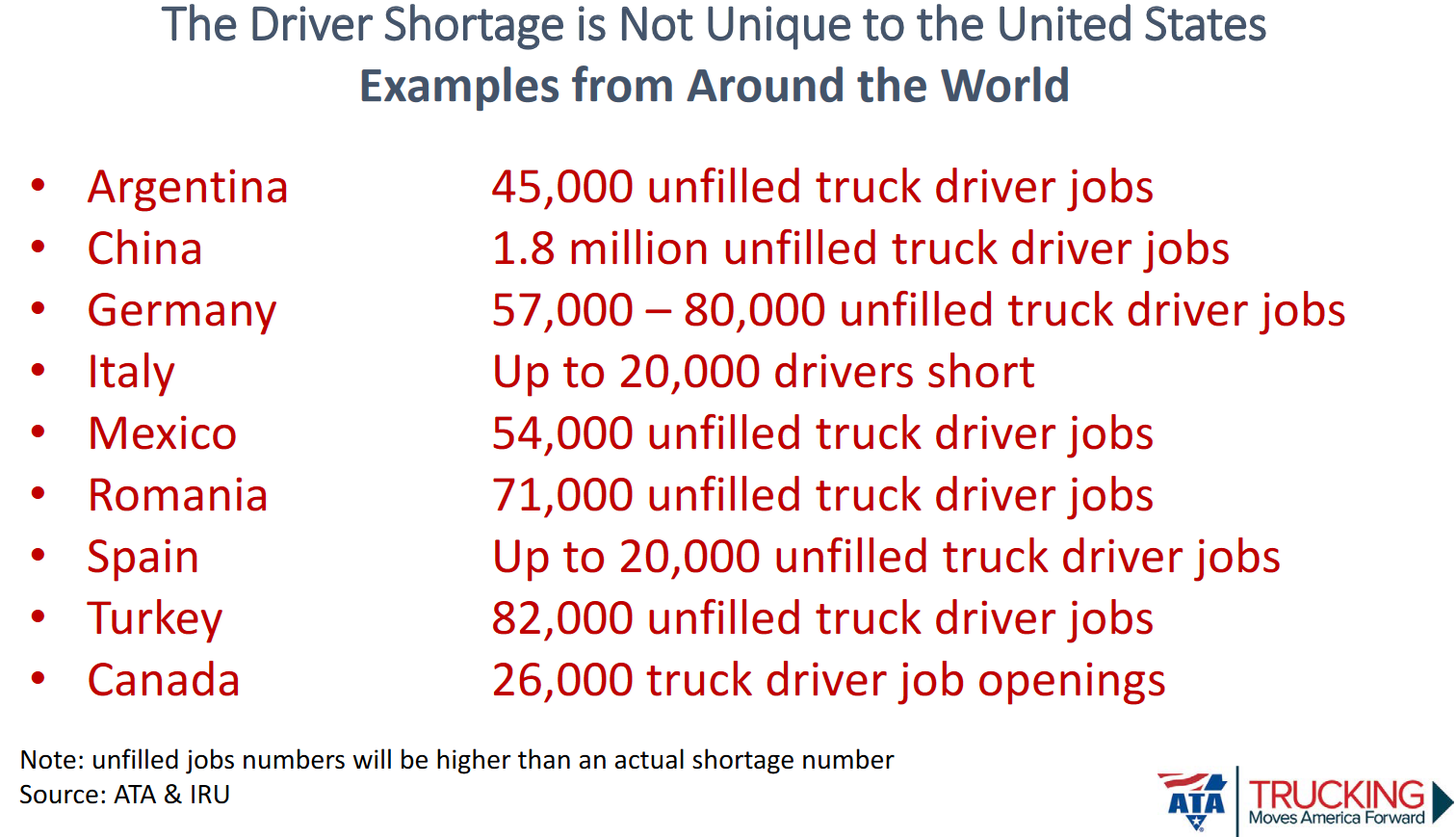

This is not a unique problem for the United States as other countries are experiencing similar trends relating to driver shortages, with China leading the way with the largest shortfall! As you review these numbers, keep in mind populations and markets are markedly smaller in comparison, therefore some of these shortages are much more problematic!

After many years of driver pay and benefits lagging counterparts in other industries, the pandemic has most assuredly impacted conditions per below:

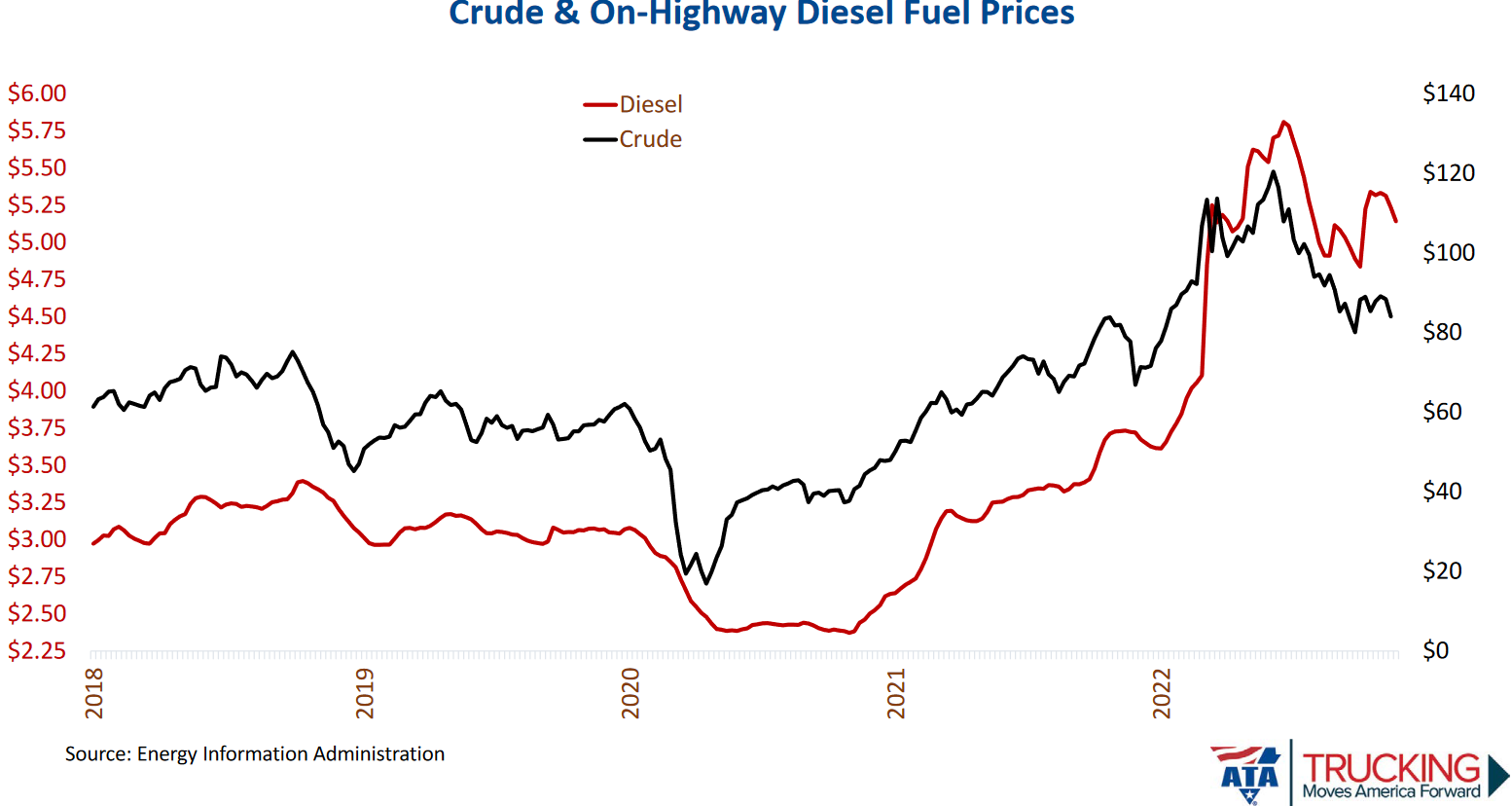

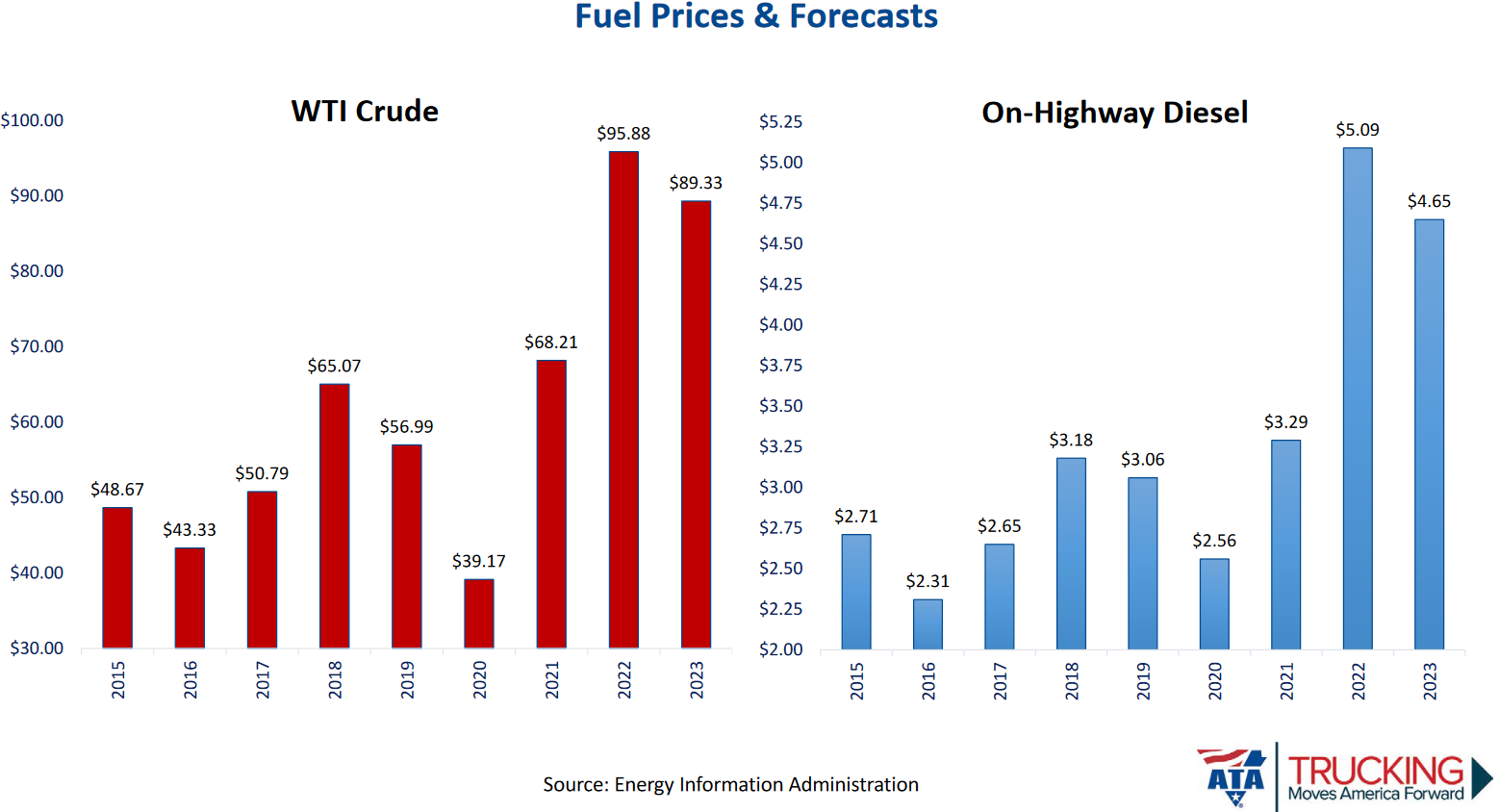

Fuel Costs – The single largest line item on fleets income statements is total fuel costs. Is it only me, but does anyone remember when diesel fuel was actually cheaper than regular gasoline? Demand for trucks and fuel being burned in comparison to gasoline demand is most likely the root cause of this adjustment. However, I can’t help but be a bit cynical regarding the large oil companies having increased their margins on diesel fuel vs gasoline, only because they could. It is yet to be seen whether that trend will continue. But I recall very well at Thanksgiving, many pundits on the news channels were predicting a diesel shortage by year end followed by exorbitant price increases. It didn’t develop, most likely as demand has declined due to freight softening.

If there is any silver linings in our review of what is in store for 2023, it could be that we will actually see some reduced costs for diesel fuel.

In any event, the oil companies prefer to have a volatile crude oil market. They actually make extraordinary amounts of money in rapidly increasing and declining crude costs. With their massive storage capabilities, the opportunity for them to build inventory in times of lower crude costs, to release and stop producing when costs are high, makes them capable of manipulating and playing the market to their advantage, as we have seen record profits in 2022 from oil companies as a result of this volatility. As supply chains continue to get more dependable, as demand and freight gets more normalized, hopefully we will see more moderate costs in diesel fuel during 2023.

Focus: The Truckload Freight Demand Component

Forecasts have been relatively consistent that demand for truckload capacity should roughly hold serve. Consumer spending has moderated a bit and housing is expected to continue its decline. However, supply chains are expected to normalize which should reduce prices in some segments of consumer spending, thereby buoying demand from a truckload volume standpoint.

Bloomberg Truck Loadings Forecast

Housing experienced a surge during 2021 and early 2022 as professionals migrated from the office to remote work and were thus, able to move to areas where their earnings stretched further. However, much of this surge took place while interest rates were historically low. Given that the rates have since risen rapidly, it has created a substantial disincentive to move and has therefore reduced demand for housing. Historically, the number of housing starts were only briefly in excess of replenishment rates and therefore, as rates subside, authentic demand should fuel a resurgence in housing demand and investment. It is, however, unlikely to occur during 2023.

Housing Starts per month (1,000’s)

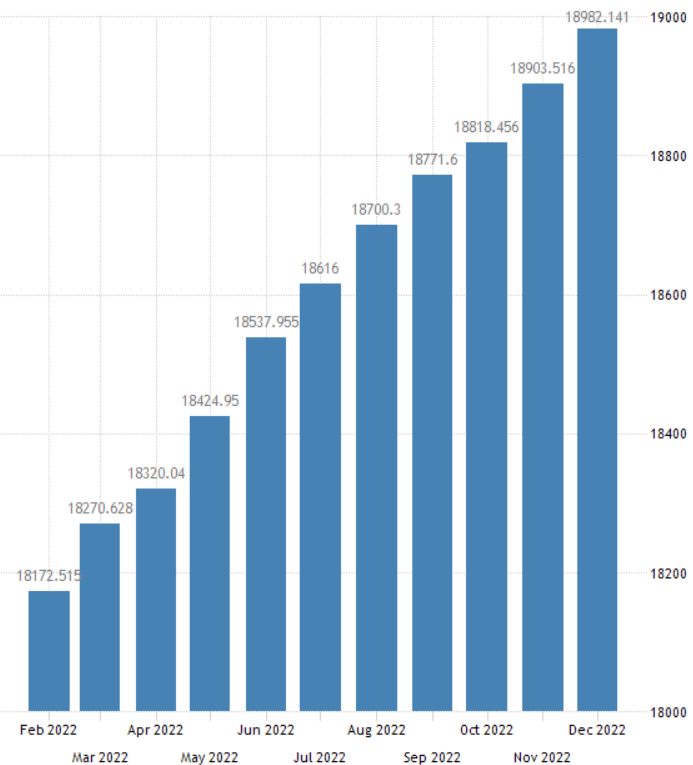

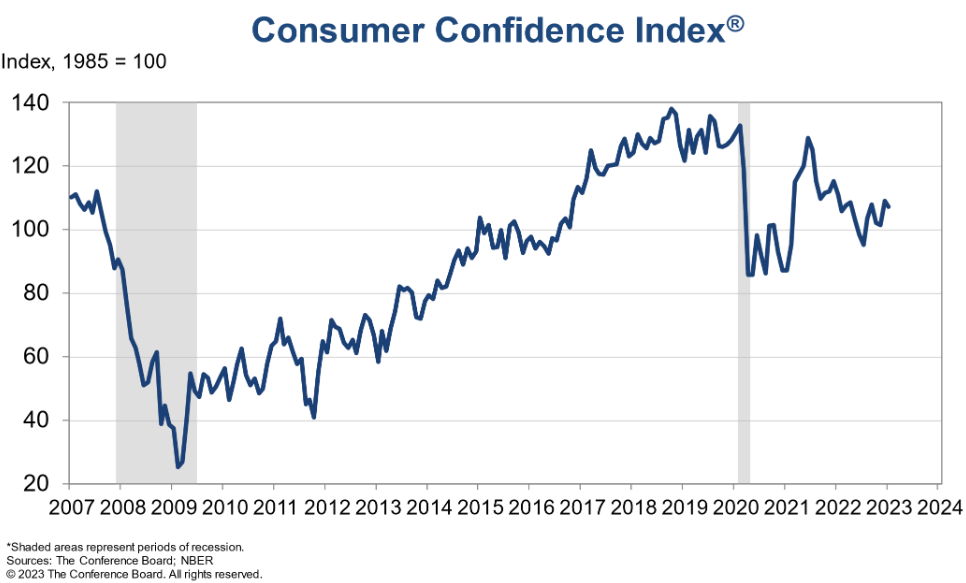

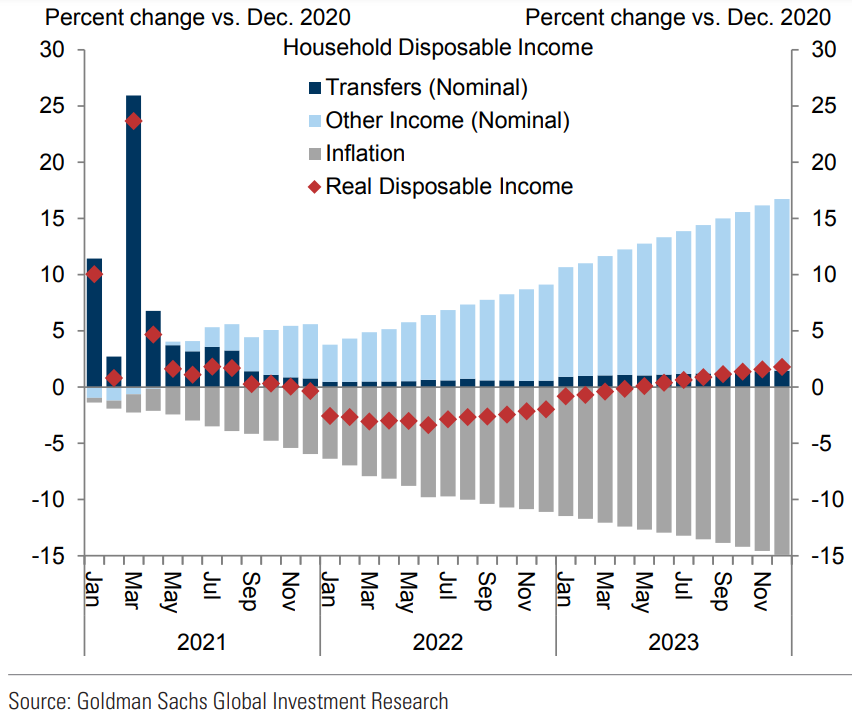

Consumer spending continued to climb throughout 2022 despite inflation outpacing wage gains and savings falling. The consumer behavior indicates consumer confidence and in fact this explains at least part of this dissonance. Disposable Personal Income continued to recover throughout most of 2022.

United States Disposable Personal Income

Many economists believe that the transitory, divergent spending behavior was more a function of new covid-era spending habits than some sort of false confidence. If this is correct, the reality of household financial pressures should have ultimately supplanted ill-conceived, synthetic spending patterns and demand waned. However, Goldman Sachs believes that this condition is more authentic, that the trend of inflation outpacing wage gains has reversed and will continue during 2023 to the extent that disposable income will rise, further supporting demand.

Focus: The Truckload Freight Supply Component

Many great general economic markets have had loose truckload freight markets and many poor general economic markets have made for tight truckload freight markets due to the truckload supply and demand range-rate of change dissonance. While the data indicates that the class 8 order peak was near the beginning of 2021, the lead time was nearly 12 months. Thus, the surge began being delivered and seated more than a year later. This corresponds precisely with the freight market’s rapid, dramatic decline that began in March of 2022. By March of 2021, orders had declined precipitously and rapidly commensurate with the declining 2022 freight market. Though the data shows a massive spike of orders at the end of 2022, this would appear misaligned with the lack of appetite to grow fleets. This surge indeed proved to be a function of continued Class 8 manufacturers’ supply constraints and leveraging those constraints for end-of-year orders. This should foretell rapid declines in orders early into 2023.

Class 8 Tractor orders are done through the end of 2023. Order slots are gone, and if companies would want to increase their fleets, order boards are almost going to make that impossible. Therefore, the freight forecasts could take some pressure off these numbers. Fleets will be refreshing their fleets as they always do during the year. However, if we were to see increased demand, surplus capacity in trucks will be difficult to find. Some fleets are having some trouble factoring in the increased financing costs due to the rapid rise in interest rates. This could affect some cancellations in current order boards, though it is not anticipated to be an impactful amount, at least for tractors. Trailers on the other hand have experienced a much wider swing in the pendulum, in that orders for trailers have been upwards of a year out, if then, with manufacturers not even committing to what the final price would be. Therefore, fleets were placing trailer orders for a set number of slots, not knowing what the eventual capital cost would be. As the spot market has waned and interest rates have risen, the trailer market seems to be adjusting faster than the tractor market, with dealers beginning to contact fleets with some availability of slots through the end of the year, reversing a frenetic pace of capital requirements and lack of availability. Tractors as compared to pre-pandemic costs are up 20 to 25 % whereas trailers have seen pricing increase from 30 to 40 % (and 50 to 60 % for specialized trailers and reefers) during the same time. Inflationary costs of these large ticket items combined with every cost in our industry increasing, has been much of the rapid rise in freight costs. As raw materials costs and demand begins to normalize, this should take some pressure off our industry that has been experiencing never seen before inflationary pressure.

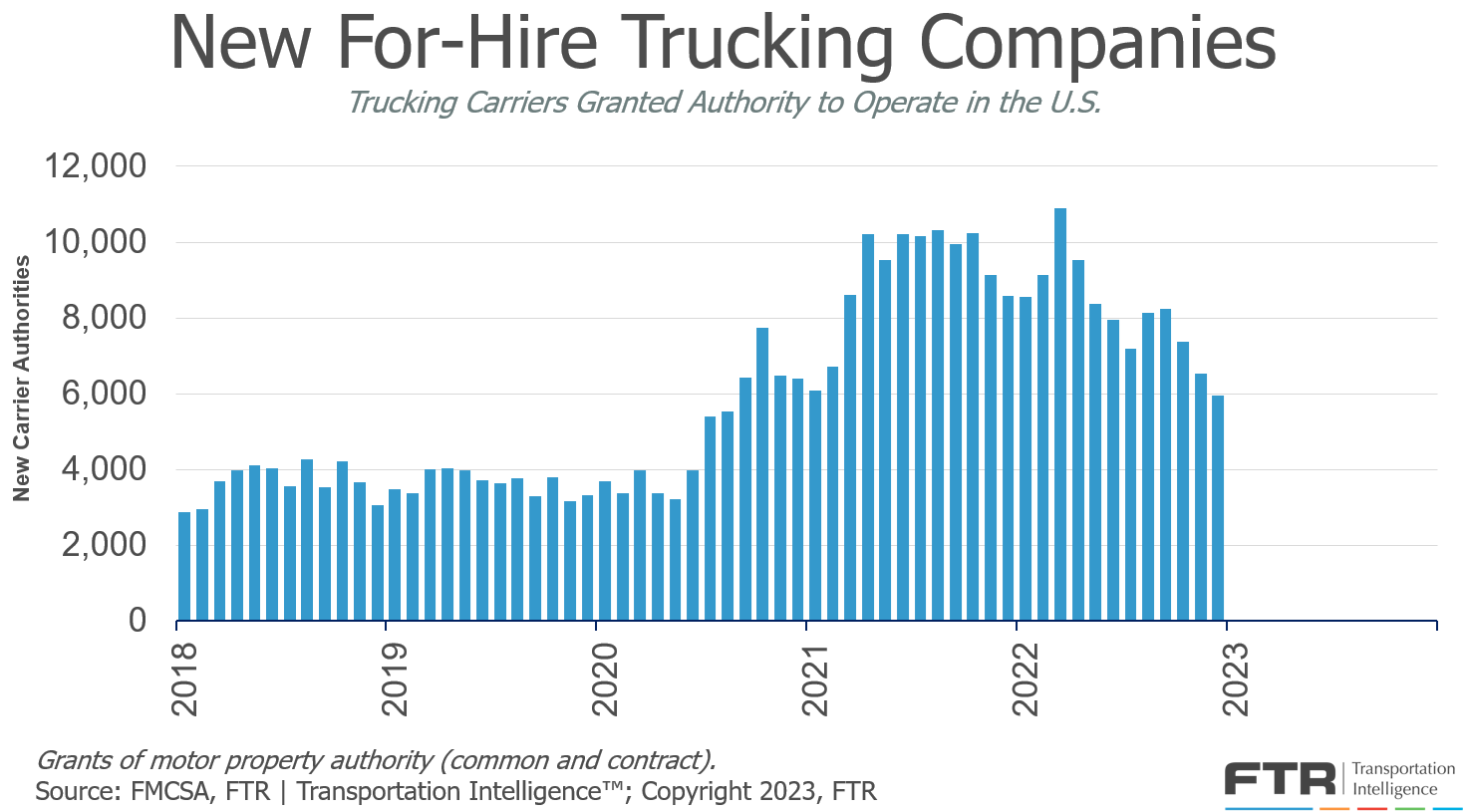

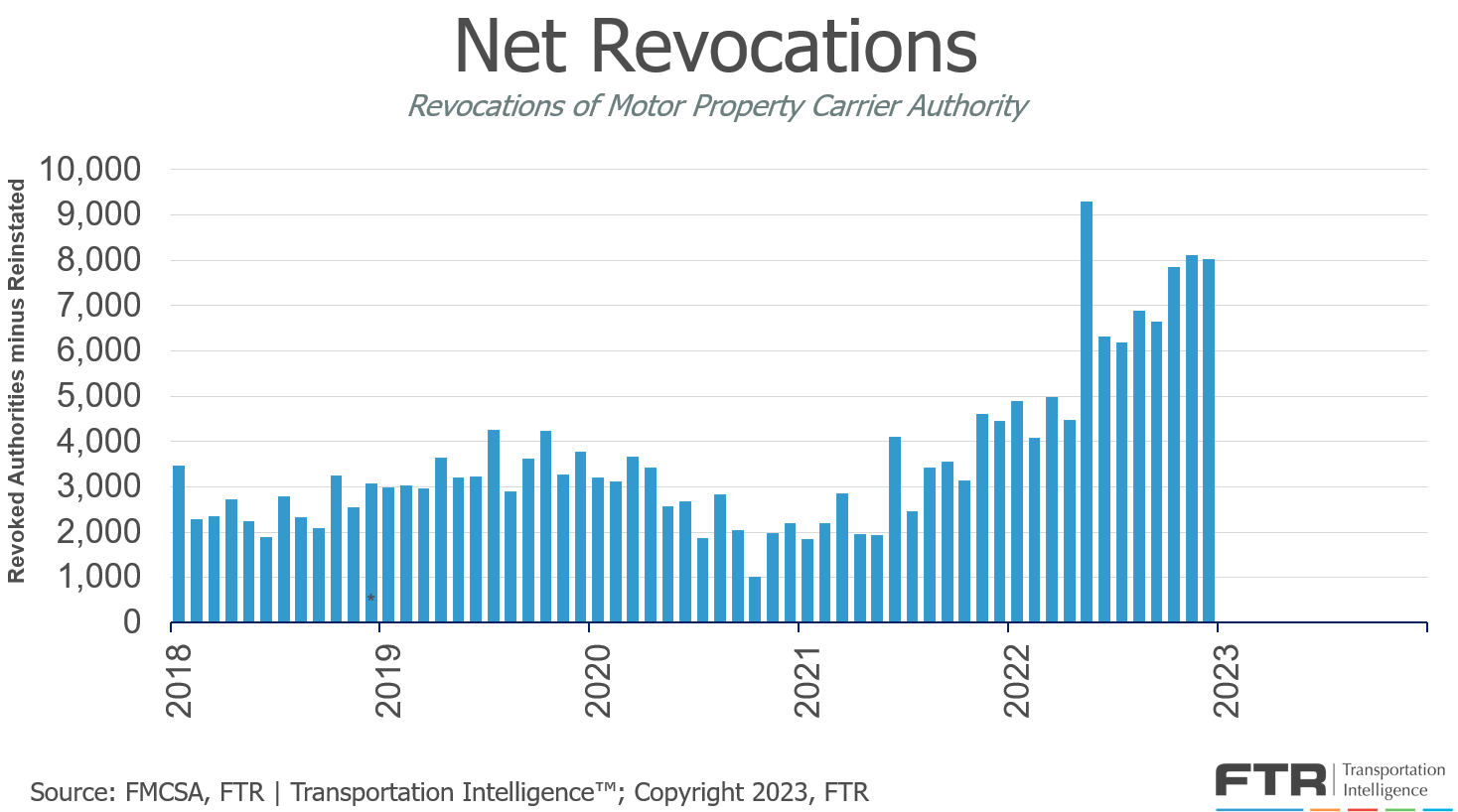

In addition to the declining supply of class 8 equipment, another unprecedented phenomenon looms. During 2021 and thru February of 2022, spot rates were at historical highs. This lured many new carriers into the market. Some were new, but others were merely transitioning from company driver to owner-operator. The demand for drivers was astronomical and many fleets attracted new drivers into the truck driving profession with sign-on bonuses and finishing schools. The substantial, rapid decline in rates reversed this trend. While many small carriers transitioned and are transitioning currently back to the company driver seat, others left the industry entirely. The fundamental yield was some significant reduction in actual capacity. The ongoing unprecedented authority revocation provides an educated idea as to the direction of truckload supply: down.

Regulations and Other Factors that Could/Shall Impact Conditions for 2023+

2023 is not expected to be a banner year for impactful legislation related to the freight market. However, there are a few noteworthy exceptions worth monitoring that could most assuredly play a significant role in how the freight industry will shape up during 2023.

Independent Contractor Classifications

California’s war on Independent Contractor status (Bill AB5) has certainly set us up for much debate and clarification during 2023. This started out as a movement to organize the ride share and food delivery services but has morphed into an all-out war of epic proportions for trucking independent contractor status as well. In the freight industry, there has historically been a strong contingent of independent contractors. They remain a very resourceful group that being independent was certainly their absolute preference from the very outset. Governmental agencies such as the Department of Labor, the National Labor Relations Board and the Internal Revenue Service have each been issuing proposals regarding their regulations within their purview after California’s passage of Bill AB5, however, nothing so far changes the current status as these issues are being left up mostly for the states to clarify rules for classification of independent contractor status. The Trump Administration attempted to simplify the “tests” for status into a two core factor of control and investment with three additional factors (integration, skill and permanency) that would arise only if the two factors are in disagreement. However, the current administration would like to return to the previous comprehensive six factor test that will only create opportunities for more lawsuits and confusion for the industry. In any event, it will not help for states to have a patchwork effect of differing laws specifying individual I/C statuses across our nation, and our industry having drivers having crossing state lines with conflicting views. It will most likely fall on the I/C’s chosen state of residence to apply initially in the classification. Needless to say, the passage of California AB5 has most definitely impacted that state with many I/C’s leaving trucking altogether, or moving to states with more favorable classification environments. This all comes at a time when we need to be inviting more drivers into the industry rather than creating more issues to resolve to continue being productive within our industry. This will not be resolved anytime soon, however, should be on the radar of everyone impacted by the freight industry as it will most certainly have long term industry impact.

FMCSA Opens Young Driver Pilot Program

On July 27, 2022, the Federal Motor Carrier Safety Administration opened applications for the new pilot program that allows younger drivers to participate in interstate commerce. The pilot program was created under last year’s Infrastructure Investment and Jobs Act, and will allow up to 3,000 younger drivers (ages 18 – 20) to undertake additional training and drive in interstate commerce.

Our industry as a whole supports allowing these younger drivers to enter the workforce, since young people have to wait until age 21 after coming out of high school to qualify to choose a driving career after not choosing the college path, then our industry has most likely lost them forever. We also acknowledge that these 18 – 20-year-olds are qualified and able to take in state driving positions of Class 8 vehicles in most jurisdictions, they just cannot legally cross state lines in interstate commerce under current federal regulations. This apprenticeship program will allow our industry to ease into this while designing comprehensive training programs for the younger set, to gain experience slowly and in a supervised environment. This has been long overdue for our industry as we continue to struggle with driver shortages, and this is a good first step in allowing our industry to recruit from a labor pool not afforded to this point that can make career choices that will greatly enhance their earning capabilities right out of high school for individuals that college is just not their career path.

Trucking Industry Opposes Federal Gas Tax Holiday

On June 23 of last year, President Biden called on Congress to pass a short-sighted three month suspension of the federal gas tax. Temporary suspension of the 18-cent per gallon federal tax on gas and 24-cent on diesel fuel would likely have a minimal impact on prices at the pump, but would result in reducing the funding of the Highway Trust Fund by $ 10 Billion and would ultimately undermine the progress made under last year’s landmark bipartisan infrastructure bill.

Our industry takes an alternative position on this option as evidenced by the comments by our President and CEO of the American Trucking Association, Chris Spear:

“After months of touting things this Administration and Congress can do that will actually make a difference. Make America energy independent and reduce our dependence upon Saudi Arabian Oil. Renew trade agreements with the European Union and the Asian Pacific nations in order to export more American oil and natural gas. And balance the budget…. Stop wasting hard-earned taxpayer dollars on senseless programs that drive up inflation and runaway deficits.

Energy independence, trade and a balanced budget. Do that, and America wins!”

Several states have granted fuel tax holidays for their state portions of fuel taxes (The state of Georgia being one), and depending upon their state highway budgets, can most likely manage their own resources, however, our industry prefers that the Federal Highway funding remain intact, as the needs for infrastructure improvements across our national system of interstates are in bad need of capital investment.

Ocean Shipping Reform Act Passage

On June 13, 2022, with bipartisan support, Congress passed the Ocean Shipping Reform Act by a 369 to 42 vote count in the House of Representatives. This bill provided important tools to address the unjustified and illegal fees being collected from American Truckers and Shippers by the ocean shipping cartel. How many of us have been charged exorbitant fees with the threat of consequences of losing our port and supply chains access for refusal. This has resulted in shipping lines raking in $ 150 Billion in profits from last year alone. These fees hurt American motor carriers and import/export companies driving record inflationary pressure. This legislation will end abusive practices imposed on us by ocean carriers that are overwhelmingly foreign owned. Many of the charges were arbitrarily charged for fees, fines, demurrage and excessive container costs, merely because they had the leverage to do so. Many of the charges were ultimately outside of the control of the carriers and shippers.

This legislation will mandate a new rulemaking by the Federal Maritime Commission to prohibit unjust and unreasonable charging practices and ensure fair practices at our ports. As America’s supply chain continues to be more dependent upon global international trade, this can only result in modernizing laws governing ocean freight and help to restore a fair marketplace for shippers and carriers so dependent upon our ports and supply chain.

Final Observations

- We will continue to see more Alt-Shoring (think Vietnam or the Philippines vs. China), Near-Shoring and Re-Shoring for manufacturing as political and cultural shifts will continue combined with risk management decisions impacting these supply chain decisions as well. This will continue to change supply chains and how freight will flow in the future.

- The economy will mostly likely experience a mini-industrial and segmental recession throughout 2023 and into 2024. Some industries will most likely be impacted more severely, some might not notice much difference at all. The one unknown will be how long and how deep. For those industries so dependent upon GDP growth and expansion, it is a prudent course to plan for careful monitoring of the developing economy and trigger points that could be indicative of where this economy could be heading, and having at the very least, a current plan, with an alternative backup plan should certain events happen. For those industries, you almost must “prepare for the worst, and pray for the best!”. However, regarding the freight industry and pockets of manufacturing, it is anticipated at least at this point, recessionary pressures could be light. The spot market portion of the industry should experience larger trough and wider impact in relation to time.

- Net revocations for smaller carriers could continue their unprecedented clip as many entered the market to take advantage of the exploding spot market pricing and demand, while at the same time, paying up for equipment and drivers. As rates in the spot market remain low, many of these entities will just not be able to survive. If indeed demand is buoyed by real wage gains, this should foretell of tightening capacity and moderately rising rates this summer.

- The fleets that can continue to prefer driver friendly freight, maintain competitive pay and benefit packages without overpaying to satisfy demand, and continue to maintain strong supportive cultures will be the winners in the long run.

- Shippers have had an opportunity to benefit from a very soft spot market throughout 2022 and this is expected to persist through the first few months of 2023. We recommend balancing the leveraging of the spot market softness with the need to secure tenable, consistent capacity and service in exiting these market conditions later this year

For help better managing a supply chain, dependable information about the trucking industry, or assistance of any kind, reach out to BR Williams today!

Download the Logistics & Trucking Industry Report 2023

About BR Williams Trucking & Logistics

BR Williams, a family-owned Trucking, Warehousing, Fulfillment & Logistics Company has been serving customers since 1958. We specialize in removing the supply chain frustrations our customers have by developing custom-made solutions. We offer nationwide transportation services through our fleet and logistics division. Our multiple fulfillment and distribution warehouses in Alabama span over 1.7 million square feet. Our core values are HONESTY, INTEGRITY, SERVICE. We still serve our first customer that was established in 1958.

To discuss your supply chain needs, please contact us online or call (800) 523-7963